The Dying Dollar: A Deeper Dive

Comprehensive Analysis of “The Dying Dollar” Causal Loop Diagram

This document provides a detailed analysis of the systems dynamics at play within the “The Dying Dollar” model. It explores the interconnected feedback loops, underlying archetypes, and key leverage points that govern the behavior of the system.

Model Explanation

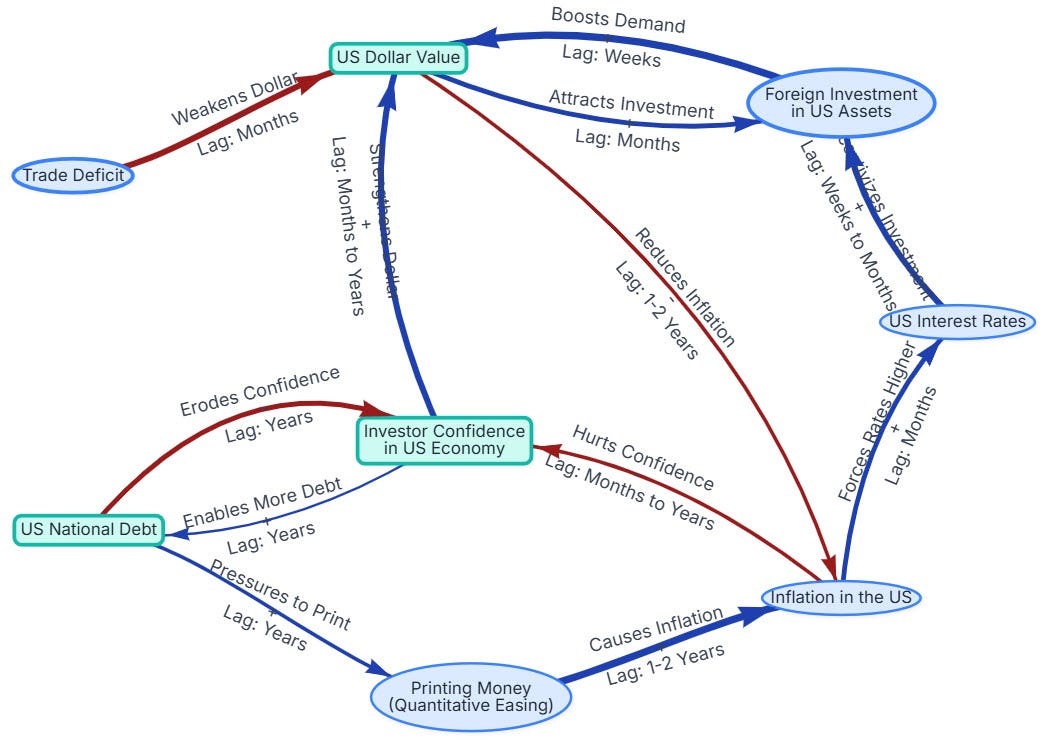

The “The Dying Dollar” model illustrates the complex interplay of factors that determine the value of the US dollar. It frames the dollar’s strength not as an isolated metric but as an emergent property of a system driven by investor confidence, national debt, trade deficits, and monetary policy.

The central dynamic explored is the United States’ reliance on Foreign Investment in US Assets to maintain the US Dollar Value, a process reinforced by the “Strong Dollar Magnet” loop (R1). This core mechanism is shown to be both a source of strength and a critical vulnerability. The model demonstrates how this reliance allows the US National Debt to grow, which in turn threatens to erode the very Investor Confidence the system depends on, creating several powerful balancing and reinforcing feedback loops that could lead to instability.

Source: The Dying Dollar (Archetypes Experimental)

Wisdom

The core wisdom of this model is that a system built on external confidence to mask internal imbalances is inherently fragile. Relying on the “Strong Dollar Magnet” (R1) to fund deficits is a short-term solution that creates a long-term vulnerability. The structure itself reveals that the longer this strategy is pursued, the more the National Debt grows, and the greater the potential for a rapid, cascading collapse should Investor Confidence falter. The true health of the currency is ultimately tied to the underlying fiscal and economic fundamentals, not just its perceived status as a safe haven.

Donella Meadows’ Leverage Points

Applying Donella Meadows’ framework helps identify the most effective places to intervene in the system, from least to most impactful.

12. Constants, Parameters, Numbers: The least effective leverage point. This would involve minor tweaks, such as trying to manage the Trade Deficit by a few billion dollars or marginally adjusting the US Interest Rates. These actions don’t change the underlying structure and are often overpowered by the system’s feedback loops.

9. The Length of Delays, Relative to the Rate of System Changes: This is a significant leverage point. The model shows long delays (years) between the growth of National Debt and the erosion of Investor Confidence. Shortening this delay—for instance, through more transparent and immediate government accounting that ties current spending to future obligations—could make the consequences of debt more visible, potentially activating the “Confidence Check” (B1) sooner and preventing excessive buildup.

7. The Gain Around Driving Positive Feedback Loops: Weakening the “Strong Dollar Magnet” (R1) or the “Confidence-Inflation Reinforcement” (R2) would be a powerful intervention. For R1, this could mean policies that encourage domestic savings and investment, reducing the reliance on foreign capital. For R2, it would mean the Federal Reserve prioritizing inflation control over asset price stability, even if it means a stronger dollar in the short term.

6. The Strength of Negative Feedback Loops: This is a key area for intervention. Strengthening the “Confidence Check” (B1) and the “Inflationary Correction” (B3) would make the system more self-regulating. For B1, this could involve creating automatic fiscal rules (like debt ceilings with real consequences) that are triggered when debt-to-GDP ratios hit certain levels, forcing a reduction in debt and bolstering confidence.

4. The Power to Add, Change, Evolve, or Self-Organize System Structure: A high-impact change would be to introduce a new balancing loop. For example, linking government spending directly to economic productivity or creating a sovereign wealth fund that uses national assets to pay down debt would fundamentally alter the system’s structure and create new self-correcting mechanisms.

2. The Goal of the System: This is one of the highest leverage points. The current implicit goal appears to be “Maintain the dollar’s status and attract foreign capital at all costs.” Changing the goal to “Achieve long-term fiscal sustainability and a balanced trade account” would force a re-evaluation of every policy within the model. It would shift the focus from managing the symptom (the need for foreign capital) to addressing the fundamental problem (the debt and trade deficits).

1. The Power to Transcend Paradigms: The highest leverage point. The dominant paradigm is that “the US dollar is the world’s unquestioned reserve currency, and deficits don’t matter because the world will always finance them.” Transcending this paradigm involves recognizing that this status is not permanent and that fundamental economic laws eventually apply to everyone. A shift in this mindset, particularly among policymakers and the public, would be the most powerful driver of change, making all other interventions more feasible.

Knowledge

The model provides specific knowledge about the relationships governing the dollar’s value:

Reinforcing Loops (Virtuous/Vicious Cycles):

(R1) A strong dollar attracts investment, which creates demand for the dollar, further strengthening it.

(R2) High confidence strengthens the dollar, which helps keep inflation low, which in turn reinforces confidence.

Balancing Loops (Corrective/Stabilizing Forces):

(B1) Rising debt eventually erodes confidence, which makes it harder to finance more debt, acting as a brake.

(B2) Confidence allows for debt, which can lead to money printing and inflation, which then destroys confidence.

(B3) A weak dollar can cause inflation, prompting higher interest rates that attract investment and strengthen the dollar.

Key Delays: The system is fraught with significant delays. It can take years for rising debt to impact confidence and for monetary policy changes (like printing money) to manifest as widespread inflation. These delays allow imbalances to grow to dangerous levels before corrective loops are triggered.

Systems Archetypes

The primary archetype at play is “Shifting the Burden.”

The Problem Symptom: A persistent Trade Deficit (n7) and the need to fund ongoing government spending.

The Symptomatic Solution: Attracting Foreign Investment (n2) by maintaining high Investor Confidence (n4) and leveraging the dollar’s reserve status. This is a quick and easy way to cover the shortfall and is reinforced by the “Strong Dollar Magnet” loop (R1).

The Fundamental Solution (Neglected): Addressing the root causes of the imbalance, such as reducing the National Debt (n3) through fiscal discipline or improving domestic economic competitiveness to close the Trade Deficit.

The Side Effect: By “shifting the burden” to foreign investors, the US is able to accumulate a massive National Debt. This creates a powerful side effect: the growing debt progressively erodes the very Investor Confidence (via B1) that the symptomatic solution relies upon. Over time, the fix itself becomes the source of a much larger, systemic problem.

Primary Principles

Structure Influences Behavior: The model shows that the current structure of global finance, with the dollar as the reserve currency, creates a system that behaves in a way that allows for massive debt accumulation.

There Is No “Away”: The debt doesn’t simply disappear. It accumulates in a stock (National Debt) that exerts influence over time on other variables like confidence and interest rates.

Feedback Loops Determine Outcomes: The long-term trajectory of the dollar will be determined by which feedback loops dominate—the reinforcing loops of confidence and investment (R1, R2) or the balancing loops of fiscal consequence (B1, B2, B3).

Delays Cause Oscillations and Overshoot: The long delays between debt accumulation and the erosion of confidence mean the system can “overshoot” its sustainable debt level significantly before corrective pressures mount, setting the stage for a more severe correction later.

Key Insights

Investor confidence is the system’s linchpin; it is both the enabler of the current dynamic and its greatest vulnerability.

The “Strong Dollar Magnet” (R1) is a double-edged sword. It provides short-term funding but creates long-term dependency and masks underlying fiscal problems.

Inflation is a potential “release valve” for unsustainable debt, but it comes at the cost of eroding confidence and devaluing the currency, as shown in loops R2 and B2.

The system is self-regulating, but the balancing loops (like “The Confidence Check”) have very long delays and may only activate forcefully during a crisis.

Future Implications

The model suggests two primary future trajectories:

The Slow Decline: The balancing loops (B1, B2, B3) exert gradual pressure. Political will slowly materializes to address the debt, inflation is managed, and the dollar’s role in the global economy diminishes in an orderly fashion over decades as other currencies rise.

The Crisis Scenario (”Doom Loop”): The reinforcing loops (R1, R2) flip from virtuous to vicious. A trigger event—a geopolitical shock, a credit downgrade, or persistent high inflation—causes a sudden drop in Investor Confidence. This weakens the dollar, which spooks more investors, causing further selling. The Fed is forced to raise rates dramatically to defend the currency, crashing the economy and making the debt impossible to service, leading to a full-blown sovereign debt and currency crisis.

Synthesis: Core Wisdom & Highest Leverage Point

The core wisdom of the model is that long-term stability cannot be achieved by relying on external perceptions to solve internal structural problems.

The highest leverage point is therefore to change the goal of the system. The focus must shift away from the short-term goal of “maintaining the dollar’s reserve status to attract foreign capital” and toward the fundamental, long-term goal of “achieving domestic fiscal and economic sustainability.” This change in objective forces a confrontation with the underlying problems of debt and deficits, moving the focus from the symptomatic solution to the fundamental one, and is the only way to avert the long-term consequences embedded in the system’s structure.