1929 Depression Repeat: A Deeper Dive

Analysis of the “1929 Depression Repeat” Causal Loop Diagram

This document provides a comprehensive systems analysis of the causal loop diagram modeling the dynamics of the Great Depression. It breaks down the model’s structure, the knowledge it contains, and the wisdom it offers for understanding complex system collapses.

Model Explanation

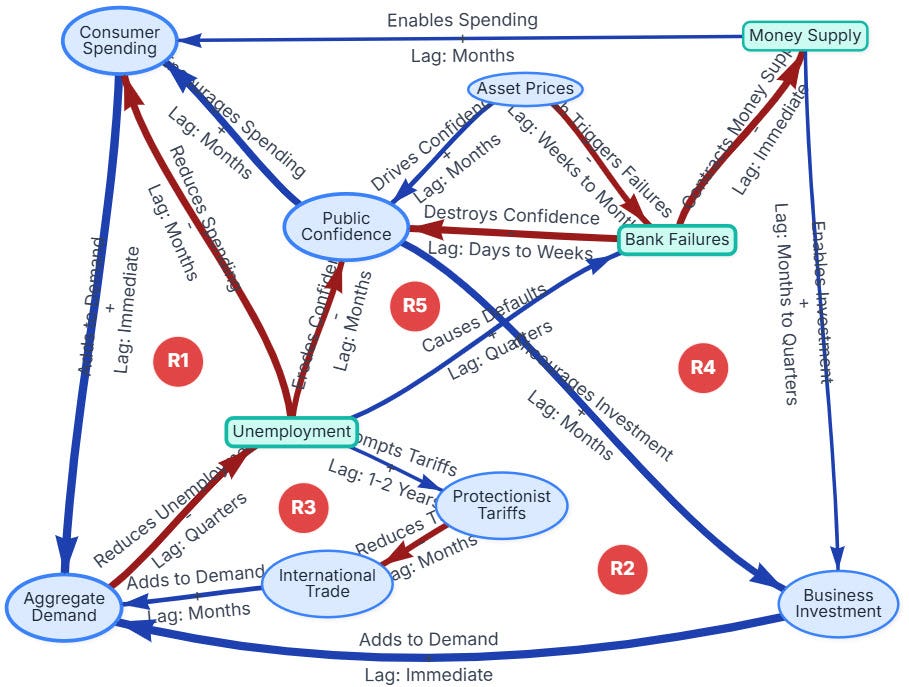

The model illustrates the catastrophic economic collapse of the Great Depression as a system of interconnected, self-reinforcing feedback loops. Unlike a stable system which has balancing loops to self-correct, this model’s structure shows how an initial shock (the 1929 stock market crash) triggered multiple vicious cycles that fed on each other, leading to a runaway downward spiral.

The core of the system revolves around three key stocks (accumulations): Bank Failures, Money Supply, and Unemployment. The behavior of these stocks is driven by variables like Public Confidence, Consumer Spending, and Aggregate Demand. The model’s narrative is one of collapse:

A fall in Asset Prices shatters Public Confidence and triggers Bank Failures.

Bank failures destroy confidence further and, critically, contract the Money Supply.

Lack of confidence and money reduces Consumer Spending and Business Investment, causing Aggregate Demand to plummet.

Falling demand leads to massive increases in Unemployment.

High unemployment feeds back to crush both confidence and consumer spending, fueling the next turn of the spiral.

A misguided policy response, Protectionist Tariffs, adds another vicious cycle by destroying International Trade and further depressing demand.

The key feature is the absence of effective balancing loops. The system’s natural self-correcting mechanisms were either too weak, too slow, or actively undermined by policy, allowing the reinforcing downward spirals to dominate and drive the economy into a deep and prolonged depression.

Source: 1929 Depression Repeat

Knowledge: The Vicious Cycles of the Depression

The knowledge embedded in the model is contained within its five reinforcing (R) loops, each representing a historically accurate “vicious cycle.”

R1: The Confidence-Spending Spiral: This loop shows the psychological heart of the collapse. As unemployment rises, public confidence erodes. Fearful people reduce their spending, which lowers aggregate demand, leading businesses to lay off more workers, further increasing unemployment and shattering confidence.

R2: The Confidence-Investment Spiral: This runs parallel to R1. As public confidence falls, businesses lose confidence in future profitability. They halt business investment, which also lowers aggregate demand, increases unemployment, and validates the initial loss of confidence.

R3: The Bank Failure Contagion: This loop shows how financial panic spreads. Bank failures destroy confidence. Lack of confidence and rising unemployment (from falling demand) lead to more loan defaults, which causes more banks to fail. This cycle is how a financial crisis “spills over” into the real economy.

R4: Monetary Contraction Spiral: This is a purely mechanical, but devastating, loop. Bank failures directly reduce the money supply. A smaller money supply makes credit scarce and expensive, choking off business investment. This leads to lower demand, higher unemployment, more loan defaults, and ultimately, more bank failures. The failure of the Federal Reserve to counteract this loop is considered a primary cause of the Depression’s depth.

R5: The Protectionist Trap: This loop demonstrates how a well-intentioned but flawed policy can create a new vicious cycle. In an attempt to protect domestic jobs, the government enacted tariffs. This triggered retaliatory tariffs, collapsing international trade. The loss of export markets reduced aggregate demand, which ultimately led to even higher unemployment—the very problem the policy was meant to solve.

Primary Principles

The model is a powerful illustration of several core systems thinking principles:

Reinforcing Feedback: The entire model is a case study in the power of reinforcing feedback to drive exponential change—in this case, exponential collapse. Each “R” loop is a vicious cycle where a decline in one area causes a cascade of effects that further exacerbate the original decline.

The Structure-Behavior Link: The structure of the system (multiple interconnected R-loops, no effective B-loops) is what produces the behavior (a deep, prolonged depression). The event of the 1929 crash was a trigger, but the resulting collapse was inherent in the system’s structure.

Policy Resistance: The “Protectionist Trap” (R5) is a classic example of policy resistance. A seemingly obvious solution (protecting local jobs with tariffs) created unintended consequences that worsened the problem, because it failed to account for the reactions of other parts of the system (retaliatory tariffs).

Systems Archetypes

Two primary systems archetypes are clearly visible and drive the model’s behavior:

Shifting the Burden: This archetype is perfectly captured by the “Protectionist Trap” (R5).

The Problem: High Unemployment.

The Symptomatic Solution: Applying “Protectionist Tariffs” to shield domestic industries. This provides a visible, immediate (though ultimately ineffective) response.

The Fundamental Solution: Fostering a healthy global economy via “International Trade,” which supports “Aggregate Demand” and creates jobs.

The Side Effect: The symptomatic solution actively undermines the fundamental solution. Tariffs lead to retaliation, which destroys international trade, further weakening aggregate demand and worsening unemployment in the long run.

Limits to Growth: While often used for growth scenarios, this archetype also explains the crash.

The Reinforcing Engine: The pre-1929 speculative bubble, driven by rising “Asset Prices” and “Public Confidence” (R1 and R2 running in a positive direction).

The Limiting Condition: The real productive capacity of the economy and the fundamental value of the assets. As the speculative bubble grew, the “limit” was approached.

The Crash: The crash was the moment the reinforcing engine reversed course violently as the system hit its limit. The balancing force (market correction) was so abrupt and severe that it kicked off all the other vicious cycles (R1-R5) in a downward direction.

Key Insights

Confidence is a Stock: The model treats “Public Confidence” as a critical variable, demonstrating that intangible psychological factors can behave like stocks in a system, driving physical outcomes like spending and employment. Its collapse was as damaging as the collapse of the money supply.

Interconnected Spirals: The Depression wasn’t caused by one thing, but by the interaction of multiple vicious cycles operating at once—a psychological spiral, a financial spiral, and a real economy spiral.

The Critical Role of the Money Supply: The model highlights the devastating mechanical link between bank failures and the money supply (R4). It shows that a financial crisis becomes an economic depression when it severely contracts the amount of money available to fuel activity.

Policy Can Create, Not Just Solve, Problems: The “Protectionist Trap” (R5) serves as a stark warning that intuitive policy responses made without understanding the whole system can create new, destructive feedback loops.

Donella Meadows’ Leverage Points

Analyzing the model through Meadows’ framework reveals why it was so hard to fix and where the most effective interventions lay.

Low Leverage (Failed Interventions):

12. Constants, parameters, numbers: Minor adjustments to interest rates were ineffective because the system’s fundamental structure was driving the collapse.

9. The length of delays: The delays between policy action and economic effect were long, making timely correction difficult.

Medium Leverage (Potential Interventions):

6. The structure of information flows: The system was plagued by panic and misinformation. A lack of transparent, credible information about the health of banks fueled bank runs. The creation of the FDIC after the Depression was a structural change to this information flow (guaranteeing deposits to prevent panic).

5. The rules of the system (incentives, punishments, constraints): The biggest rule change that came out of the Depression was deposit insurance (FDIC). This single rule change fundamentally alters the structure by severing the link between bank failures and widespread public panic (the R3 loop). Another rule change was the separation of commercial and investment banking (Glass-Steagall).

4. The power to add, change, evolve, or self-organize system structure: This refers to adding new balancing loops. The New Deal programs (like the WPA) can be seen as an attempt to create a new balancing loop: as Unemployment rises, Government Spending increases, which boosts Aggregate Demand and counteracts the fall. This was a structural change.

High Leverage (The Ultimate Solutions):

2. The goal of the system: The goal of the system pre-1929 was largely seen as maintaining a laissez-faire market with a balanced government budget. The Depression forced a shift in this goal toward maintaining economic stability and full employment, even at the cost of government deficits.

1. The paradigm out of which the system arises: This is the highest leverage point. The shared mindset of the era was that markets were self-correcting and government intervention was generally harmful. The Great Depression shattered this paradigm. The new paradigm that emerged (Keynesian economics) held that the government had a crucial role and responsibility to intervene to manage aggregate demand and stabilize a volatile economy. This paradigm shift is what enabled the structural and goal changes that followed.

Future Implications

The model remains profoundly relevant. The 2008 financial crisis saw a similar threat of cascading bank failures and a collapsing money supply. However, policy response was drastically different precisely because the lessons from the 1929 model had been (partially) learned:

Central banks aggressively expanded the money supply to prevent the Monetary Contraction Spiral (R4).

Governments used stimulus packages to directly support Aggregate Demand, creating a balancing loop to counter the Confidence-Spending Spiral (R1).

Deposit insurance prevented widespread bank runs, defanging the Bank Failure Contagion loop (R3).

The model warns of future risks. A rise in protectionism could reactivate the “Protectionist Trap” (R5). The formation of new asset bubbles (in housing, crypto, or stocks) could again create a “Limits to Growth” scenario where a crash triggers the interconnected vicious cycles. The model’s primary implication is that the stability of a modern economy depends on maintaining the strength and responsiveness of its institutional balancing loops.

Synthesis: The Wisdom and the Leverage

The core wisdom of this model is that the resilience of a complex system lies not in preventing shocks, but in its capacity to self-correct through balancing feedback loops. The Great Depression was not merely a large shock; it was a systemic failure where the balancing loops were absent, weak, or actively undermined. This allowed multiple reinforcing vicious cycles to lock in and drag the entire system into a prolonged state of collapse.

The highest leverage point, therefore, was and remains the paradigm. The belief system that markets are inherently stable and self-regulating led to policies (or lack thereof) that allowed the collapse to happen. The profound shift in thinking—to a paradigm where complex economies are understood to be inherently unstable and require active management and robust safety nets—was the most powerful intervention. It enabled the creation of the institutional balancing loops (like the FDIC and automatic stabilizers) that have, to date, prevented a repeat of the 1929 catastrophe.